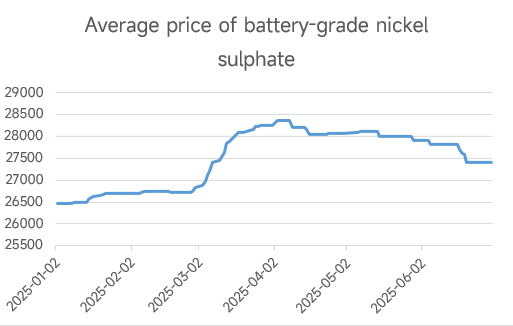

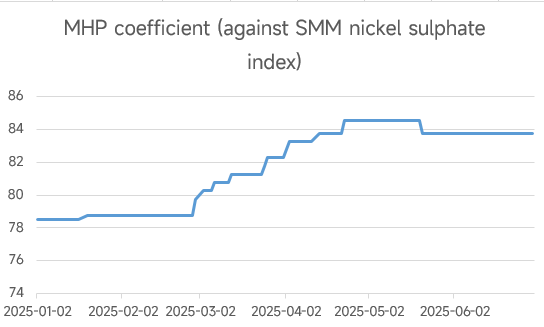

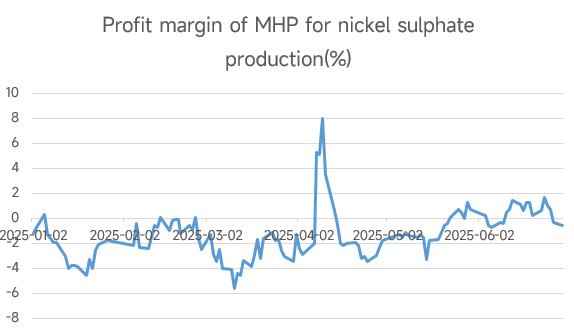

In Q1, the rising prices of MHP, coupled with a supply deficit, led to a continuous increase in nickel sulphate prices.

The expectation of a nickel ore supply deficit in Indonesia during Q1 drove the continuous rise in LME nickel prices. Meanwhile, there were also production cuts in high-grade nickel matte in Indonesia, leading to an increase in the demand for MHP by nickel salt smelters, which in turn drove up the MHP coefficient and increased the production costs of nickel salt smelters. As the losses from raw material cost inversions intensified, more nickel salt smelters chose to halt or reduce production due to losses, resulting in a significant decline in market supply. The nickel salt smelters still in production showed a strong reluctance to budge on prices. Although downstream demand in Q1 was disrupted by the Chinese New Year and fell short of Q4 last year, the shortage of raw material supply compelled precursor manufacturers to passively accept high-coefficient raw materials, leading to a continuous rise in nickel sulphate prices.

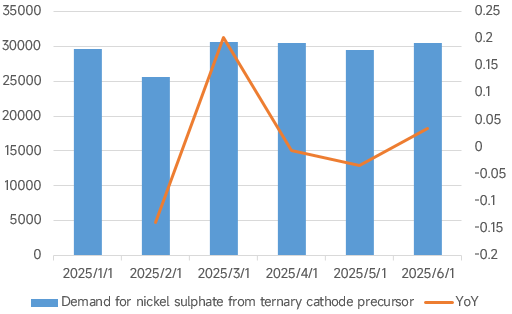

In Q2, demand slightly recovered, costs rose slightly, and nickel sulphate prices increased slightly.

From the perspective of nickel price performance, LME nickel prices showed a downward trend in Q2, mainly due to the disruption caused by US tariff policies. At the same time, floods in Indonesia affected MHP production, leading to a MoM decline in MHP production in Q2. The reduction in supply and the failure to resume production of high-grade nickel matte, which could not serve as a raw material substitute for MHP, pushed the MHP coefficient slightly higher, thereby driving up the overall production costs of nickel salts. On the demand side, with the recovery of production days, downstream precursor manufacturers' demand for nickel salts increased slightly compared to Q1. However, due to the overall weak demand for ternary materials, the incremental space for nickel salt demand was limited. On the supply side, the upward trend in raw material prices led to a strong reluctance to budge on prices among nickel salt producers. However, due to the still weak downstream demand, the upward range of nickel salt prices was suppressed. Overall, under the dual influence of a slight recovery in demand and an upward trend in costs, nickel salt prices showed a slight upward trend in Q2.